PA BHPH Regs Decoded: Stay Compliant Or Risk Penalties

- 01. PA BHPH loan regulations decoded: core obligations

- 02. Key Pennsylvania statutes affecting BHPH

- 03. Federal rules that apply to PA BHPH dealers

- 04. Common BHPH regulatory pitfalls in Pennsylvania

- 05. Compliance checklist: must-do items for PA BHPH dealers

- 06. Step-by-step compliance workflow for new deals

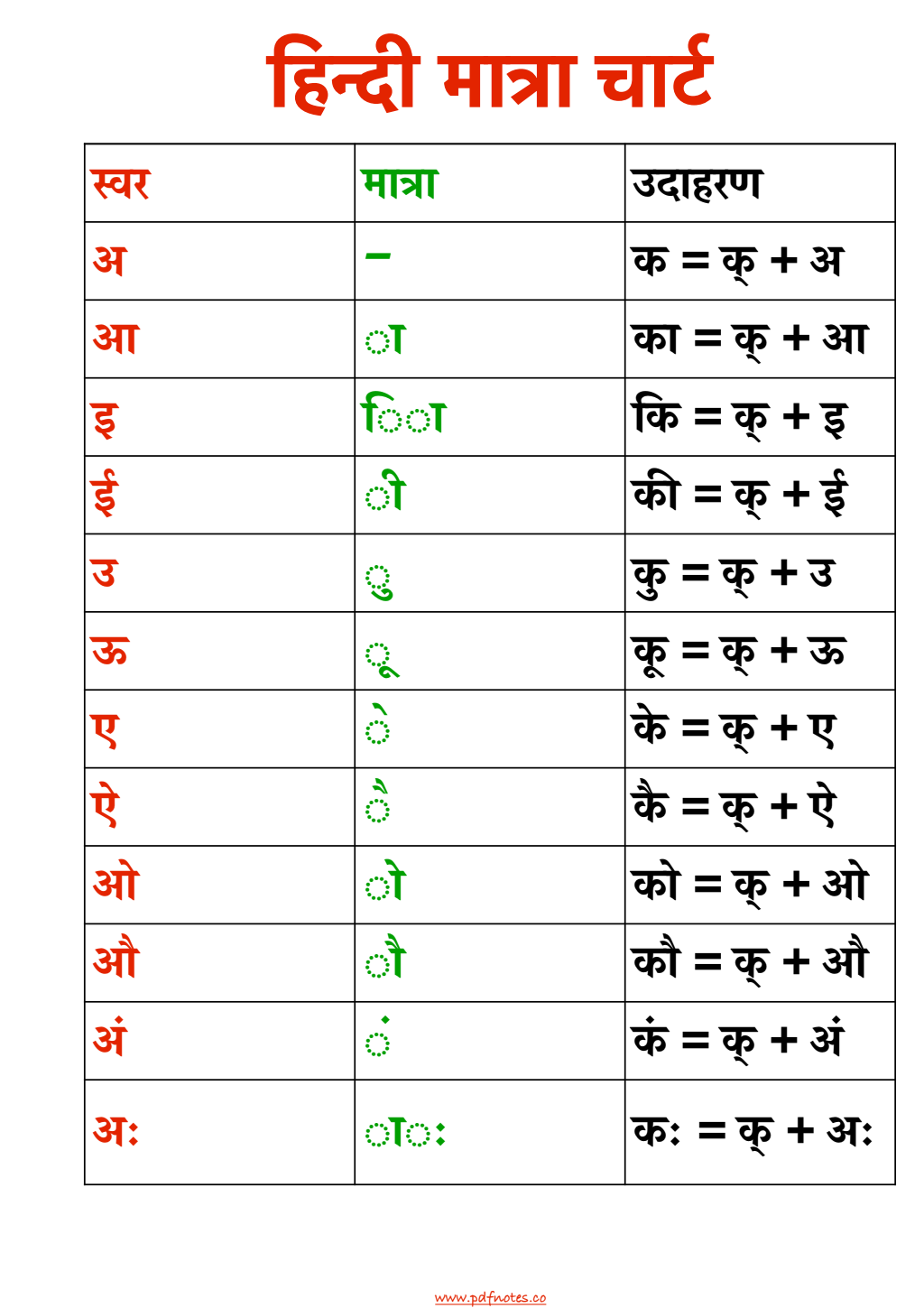

- 07. Illustrative BHPH compliance table for Pennsylvania

- 08. Recommended internal controls and training

- 09. Enforcement and penalties in Pennsylvania

PA BHPH loan regulations decoded: core obligations

Buy-here-pay-here (BHPH) loan regulations in Pennsylvania are governed by a mix of state consumer-finance statutes, general motor-vehicle sales laws, and the same federal lending rules that apply nationwide, including the Truth in Lending Act (TILA) and the Fair Credit Reporting Act (FCRA). For a BHPH dealership, the bottom line is that you must have a valid dealership license from the Pennsylvania Motor Vehicle Advisory Board, comply with state-level interest-rate ceilings unless you qualify for an exemption, and follow all federal disclosure and fair-lending requirements on every retail installment contract.

Key Pennsylvania statutes affecting BHPH

Pennsylvania's usury law caps finance charges on consumer loans, but BHPH dealers often fall under exemptions when they originate motor-vehicle financing contracts as a dealer-lender rather than a traditional bank. Even so, the Commonwealth's Consumer Credit Code still imposes disclosure duties, limits on deceptive practices, and certain restrictions on late-fee structures and balloon-payment terms. If the dealer's financing arm is structured as a separate finance company, it may also need to register as a sales finance company or similar entity under state financial-services law.

The Pennsylvania Motor Vehicle Sales Finance Act requires that every retail installment contract for a motor vehicle contain specific items such as the total amount financed, the annual percentage rate (APR), the total of payments, and the schedule and method of payment. This statute also ties into repossession rules, requiring enforcement of repossession procedures that do not "breach the peace" and that comply with notice and redemption requirements.

Federal rules that apply to PA BHPH dealers

Federal legislation shapes Pennsylvania BHPH activity in critical ways. The Truth in Lending Act mandates that dealers provide a standardized finance-charge disclosure, including the APR, the total finance charge, and the number and amount of payments, on every consumer loan. The Fair Credit Reporting Act requires that dealers report accurate information to credit reporting agencies and handle adverse-action notices properly when an applicant is denied credit or offered worse terms based on a credit report.

Additional federal guardrails include the Fair Debt Collection Practices Act (FDCPA), which controls how dealers may attempt to collect delinquent motor-vehicle payments, and the Equal Credit Opportunity Act (ECOA), which prohibits discrimination in loan approvals based on race, gender, age, or other protected characteristics. The Consumer Financial Protection Bureau has also signaled increased scrutiny of BHPH practices, including high-interest subprime loans and aggressive repossession tactics.

Common BHPH regulatory pitfalls in Pennsylvania

Several recurring issues place Pennsylvania BHPH dealers at risk of civil penalties or enforcement actions. These include under-disclosing the total finance charge on retail installment contracts, failing to deliver a properly itemized Truth in Lending disclosure at or before consummation, and using unclear or misleading advertising that misstates the APR or payment amount. Some dealers also run afoul of Pennsylvania's consumer-protection statute by rolling excessive fees into the contract or by misrepresenting the vehicle's condition or mileage.

Another frequent problem is noncompliant repossession practices. Pennsylvania law does not allow dealers to repossess a vehicle in a way that breaches the peace, such as by removing personal property from a locked garage or using force against a customer. Post-repossession, failure to promptly notify the consumer of the deficiency balance or to properly account for the sale of the repossessed vehicle can trigger liability under the Motor Vehicle Sales Finance Act.

Compliance checklist: must-do items for PA BHPH dealers

- Obtain and maintain dealership licensing: Ensure both sales and any in-house finance operations are covered under current Pennsylvania Motor Vehicle Advisory Board rules.

- Disclose all finance charges clearly: Use a standardized TILA disclosure that itemizes the APR, amount financed, total finance charge, and payment schedule.

- Verify contract accuracy: Confirm that every retail installment contract reflects the agreed-upon terms, including fees, rebates, and any add-ons.

- Enforce fair-lending practices: Under ECOA, document underwriting decisions and avoid steering or pricing based on protected characteristics.

- Track repossession legality: Train staff to avoid any act that could be deemed a breach of the peace during repossession.

- Secure proper consumer consents: Obtain written consent for credit checks and clearly disclose how credit information will be used.

- Control advertising claims: Ensure all marketing for BHPH financing is accurate and does not mislead on interest rates, down payments, or approval guarantees.

Step-by-step compliance workflow for new deals

- Pre-approval screening: Conduct a documented credit, income, and debt-to-income review consistent with state and federal fair-lending rules.

- Rate and term determination: Set APR and fees within Pennsylvania's usury limits or applicable dealer-finance exemptions.

- Prepare disclosures: Generate the TILA disclosure, itemized contract, and any state-specific forms required by the Motor Vehicle Sales Finance Act.

- Customer review and signing: Allow the customer to examine disclosures in ink or electronic form and obtain dated signatures.

- Record retention: File executed contracts and disclosures in a secure system that supports audits and potential regulatory requests.

- Payment processing and monitoring: Track delinquencies and communicate with the consumer in a manner compliant with the Fair Debt Collection Practices Act.

- Repossession documentation: If repossession becomes necessary, document every step, including notice, valuation, and sale of the repossessed vehicle.

Illustrative BHPH compliance table for Pennsylvania

| Compliance Area | Relevant Rule or Law | PA-Specific Note |

|---|---|---|

| Interest-rate caps | Pennsylvania usury law and Consumer Credit Code | Dealers may benefit from motor-vehicle finance exemptions, but still must disclose APR and total finance charge. |

| Loan disclosures | Federal Truth in Lending Act (TILA) | Mandatory APR, payment schedule, and total of payments on every retail installment contract. |

| Fair lending | Equal Credit Opportunity Act (ECOA) | Prohibits discrimination; requires adverse-action notices when applicable. |

| Consumer reporting | Fair Credit Reporting Act (FCRA) | Dealers must use accurate credit data and follow dispute procedures. |

| Repossession | Pennsylvania Motor Vehicle Sales Finance Act | Repossession must not breach the peace and must include proper notice and accounting. |

| Debt collection | Federal Fair Debt Collection Practices Act (FDCPA) | Applies to collection agencies and in-house collectors; restricts abusive tactics. |

| Advertising | FTC Used Car Rule and state consumer-protection law | Advertising for BHPH financing must not misstate terms or approval odds. |

Recommended internal controls and training

Strong internal controls are essential for consistent compliance with Pennsylvania BHPH loan regulations. Dealers should implement a documented compliance policy that assigns responsibility for reviewing contracts, training staff, and conducting periodic audits of executed retail installment contracts. At least annually, a compliance officer should sample 5-10% of new contracts to verify that finance-charge disclosures, APRs, and payment schedules match the advertised terms.

Training programs should cover several key topics: how to explain APR and total finance charge disclosures to customers in plain language, how to avoid any conduct that could be viewed as a breach of the peace during repossession, and how to handle collection contacts in a way that complies with FDCPA and ECOA. Real-world scenarios, such as handling a consumer complaint about unexpected fees or responding to a disputed repossession, should be role-played to reinforce proper behavior.

Enforcement and penalties in Pennsylvania

Violations of Pennsylvania BHPH loan regulations can trigger investigations from multiple agencies, including the Pennsylvania Attorney General's Office, the Motor Vehicle Advisory Board, and the Federal Trade Commission or Consumer Financial Protection Bureau if federal lending rules are implicated. In a 2023 sweep targeting high-cost motor-vehicle financing practices, several Northeastern dealerships were fined between $50,000 and $300,000 for systematic TILA disclosure failures and deceptive advertising claims about no-credit-check approvals.

Penalties can include civil fines, restitution to affected consumers, mandatory corrective advertising, and in some cases, suspension or revocation of a dealer's motor-vehicle license. In extreme situations involving repeated or intentional violations, individual officers may face personal liability or referrals for criminal prosecution, particularly where consumer-fraud statutes or falsification of credit information are implicated.

Expert answers to Pa Bhph Regs Decoded Stay Compliant Or Risk Penalties queries

What is the maximum interest rate a BHPH dealer can charge in Pennsylvania?

Pennsylvania's usury law sets a general cap on consumer loan interest rates, but BHPH dealers who originate motor-vehicle financing contracts often qualify for exemptions under the Consumer Credit Code and related statutes. Even when exempt from the strict usury cap, dealers must still comply with TILA's requirement to disclose the APR and total finance charge, and must avoid practices that state regulators deem "unconscionable" or predatory.

Do BHPH dealers in Pennsylvania need a separate finance license?

If a Pennsylvania BHPH operation separates its in-house financing arm into a distinct finance company, that entity may need to register as a sales finance company or similar nonbank lender under state financial-services law. The requirement depends on factors such as whether the company holds multiple contracts, takes assignments of dealer contracts, and meets certain thresholds for consumer lending. Many full-service dealerships, however, structure financing as an extension of the dealership and operate under the existing motor-vehicle dealer license.

Are repossession rules different for BHPH loans in Pennsylvania?

The repossession rules for BHPH loans in Pennsylvania follow the same core principles as other motor-vehicle financing contracts governed by the Motor Vehicle Sales Finance Act. The key requirement is that the repossession not "breach the peace," which includes refraining from threats, physical force, or removing a vehicle from a locked structure without the owner's consent. After repossession, the dealer must provide notice of the sale of the repossessed vehicle and properly account for any deficiency balance owed by the consumer.

What must be included in a BHPH loan disclosure in Pennsylvania?

In Pennsylvania, every BHPH retail installment contract must include, at minimum, the amount financed, the APR, the total finance charge, the total of all payments, and the number and amount of scheduled payments. These items are required by the federal Truth in Lending Act as well as Pennsylvania's Motor Vehicle Sales Finance Act. Additional disclosures may be required if the contract includes add-ons such as extended warranties, service contracts, or credit-insurance products.

Can Pennsylvania BHPH dealers advertise "no credit check" approvals?

Pennsylvania BHPH dealers may indicate that they consider alternative underwriting factors, but they must avoid advertising that implies total disregard for credit and misleads consumers about their approval odds. Claims such as "no credit check" can draw scrutiny under the Consumer Credit Code and FTC Used Car Rule if they are not substantiated or if they omit the fact that the dealer may still review employment history, income, or other indicators of creditworthiness. Any advertising language about approvals should be clear, balanced, and consistent with actual underwriting practices.

What are the consumer-protection rights of BHPH borrowers in Pennsylvania?

BHPH borrowers in Pennsylvania retain several important consumer-protection rights. They have the right to receive clear, accurate disclosures of the APR and finance charges upfront, to challenge inaccurate information reported to credit reporting agencies, and to be treated fairly during collection and repossession efforts. If a dealer violates the Motor Vehicle Sales Finance Act, the Consumer Credit Code, or federal lending statutes, consumers may be entitled to refunds, damages, or other remedies under Pennsylvania law or the relevant federal act.